1. Crunching the Numbers: The Breakeven Yield Formula Explained

In the world of finance and banking, understanding breakeven yield is essential for decision-makers looking to navigate the complexities of product marketing. Breakeven yield is a critical concept that determines the point at which the revenue generated from a product or service equals the cost of marketing it. In simpler terms, it's the point at which a financial institution neither makes a profit nor incurs a loss. In this article, we'll delve deeper into breakeven yield, exploring its significance, applications, and how it influences the financial landscape.

2. What Is Breakeven Yield?

Breakeven yield, at its core, is the yield required to cover the cost of marketing a banking product or service. It's the delicate balance where the money generated by selling a product or service equals the cost incurred to market it. In other words, it's the point of equilibrium where profit and loss cancel each other out, making it a pivotal metric for financial institutions.

3. Key Takeaways

Before we dive deeper into breakeven yield, let's summarize the key takeaways:

-

Breakeven yield is the yield required to cover the cost of marketing a banking product or service.

-

It provides decision-makers with insights into the minimum volume needed to earn a specific rate of return on a product or service.

-

The calculations involved in determining breakeven yields for loan products are relatively straightforward.

Now, let's explore how breakeven yield is understood and applied in the banking industry.

4. Understanding Breakeven Yield in Banking

In the banking world, breakeven yield offers decision-makers valuable insights into the minimum volume required to achieve a specific rate of return on a product or service. To put this into perspective, consider the various products and services offered by commercial banks to individuals and small businesses.

These offerings include:

- Deposits

- Checking accounts

- Business loans

- Personal loans

- Mortgage loans

- Certificates of Deposit (CDs)

- Savings accounts

Banks generate revenue by capitalizing on the spread between the interest they pay on deposits and the interest they earn on loans. This financial maneuver is commonly referred to as net interest income. In practical terms, customer deposits into checking, savings, money market accounts, and CDs provide banks with the capital needed to issue loans.

Providing loans, in turn, allows financial institutions to earn interest income from borrowers. These loans can encompass a wide range, from mortgages and auto loans to business and personal loans. The key to profitability lies in the fact that the interest rate paid by the bank on borrowed funds is lower than the rate charged on loans, resulting in a profitable yield.

Typically, calculating breakeven yields for loan products involves a series of straightforward calculations. It entails adding interest expenses to non-interest expenses, subtracting this sum from non-interest income, and then dividing the result by earnings assets.

5. Breakeven Yield and Additional Yield Calculations

While breakeven yield is vital in the context of bank profitability, it's not the only type of yield calculation used in finance. For instance, investors rely on various yield calculations when determining the value of bonds. Here are a few common ones:

Nominal Yield

Nominal yield represents a bond's coupon rate and is the interest rate (to par value) that the bond issuer promises to pay bondholders. This yield is fixed and remains constant throughout the bond's life. It's often referred to as nominal rate, coupon yield, or coupon rate.

Current Yield

Slightly more intricate, the current yield is the annual income derived from an investment, such as interest or dividends, divided by the security's current market price. This can be expressed as follows:

Current Yield=Annual Cash Inflows / Market Price

Current yield provides investors with a snapshot of the return they can expect if they were to purchase the bond and hold it for a year. It's important to note that it doesn't represent the actual return upon maturity.

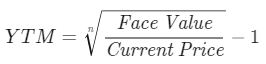

Yield to Maturity

Yield to Maturity (YTM) is a comprehensive return calculation expressed as an annual rate. It signifies the total return an investor can anticipate if the bond is held until it matures. Essentially, it's the internal rate of return (IRR) of a bond if all payments are made as scheduled and reinvested at the same rate.

The formula to calculate YTM for a discount bond bears a resemblance to IRR and is expressed as follows:

In this formula:

- 'n' stands for the number of years to maturity.

- 'Face value' represents the bond's maturity value or par value.

- 'Current price' is the bond's current market price.

6. Conclusion

In the realm of banking, breakeven yield serves as a fundamental metric for determining the equilibrium point between revenue and marketing costs. It's a critical tool for decision-makers seeking to understand the minimum volume required to achieve a specific rate of return on their financial products and services.

Moreover, beyond the banking industry, different yield calculations play a crucial role in evaluating the value of bonds, providing investors with valuable insights into their potential returns.

In conclusion, breakeven yield is a cornerstone concept in finance and banking, allowing institutions to make informed decisions and optimize their profitability. Understanding these yield calculations equips both banking professionals and investors with the knowledge they need to thrive in the complex world of finance.

7. Why should professionals use ACC Law Firm's capital Service?

-

Expertise in Legal Matters: ACC Law Firm specializes in legal services, providing professionals with access to experienced attorneys who can offer valuable legal guidance. Whether it's contract negotiations, intellectual property issues, employment matters, or any other legal concern, their expertise can be invaluable.

-

Tailored Legal Solutions: ACC Law Firm understands that every professional's needs are unique. They can customize their legal services to address the specific challenges and opportunities faced by professionals in different fields.

-

Risk Mitigation: Legal issues can pose significant risks to professionals and their businesses. ACC Law Firm can help identify and mitigate these risks, reducing the potential for costly legal disputes or compliance issues.

-

Resource Optimization: Professionals can save time and resources by outsourcing their legal needs to ACC Law Firm. This allows them to focus on their core competencies and business objectives, while leaving legal matters in the hands of professionals.

-

Access to a Network: ACC Law Firm may have a network of legal experts and professionals in various fields, which can be beneficial for clients seeking connections and advice beyond just legal services.

Q&A

Question 1: What is breakeven yield, and why is it important for businesses?

Answer 1: Breakeven yield, in a business context, is the minimum yield or rate of return that an investment, project, or product must generate to cover its costs and break even. It's essential for businesses as it helps determine the point at which their investments or activities become financially viable.

Question 2: How is breakeven yield calculated, and what is the formula for it?

Answer 2: Breakeven yield is calculated using the following formula:

Breakeven Yield = Total Costs / Investment or Sales

Where:

- Total Costs represent all the expenses associated with the investment or project.

- Investment or Sales is the amount of capital invested or the total sales revenue generated by the investment or project.

Question 3: What are the key components involved in calculating breakeven yield, and how does it vary for different types of investments or projects?

Answer 3: The key components in calculating breakeven yield include:

- Total Costs: This encompasses all costs related to the investment, such as production costs, operating expenses, and any financing costs.

- Investment or Sales: This refers to the total capital invested in the project or the sales revenue generated by it.

The variation in breakeven yield calculation depends on the specific nature of the investment or project and the associated costs. For instance, a manufacturing project would have different cost components than a software development project.

Question 4: How is the concept of breakeven yield applied in decision-making and financial planning for businesses?

Answer 4: Breakeven yield is applied in decision-making and financial planning in the following ways:

-

Investment Evaluation: Businesses use it to assess the feasibility of new projects or investments by comparing the expected yield to the breakeven yield.

-

Pricing Strategies: It helps determine the minimum pricing required to cover costs and achieve profitability.

-

Risk Assessment: Understanding breakeven yield helps evaluate the financial risk associated with an investment and the potential impact of cost overruns.

-

Performance Monitoring: Businesses regularly compare actual yields to breakeven yields to assess whether they are on track to meet their financial goals.

Nội dung bài viết:

Bình luận